Social Security, one of the most enduring government programs for retirees, has evolved over its 90-year history. As our population ages, concerns grow about whether Americans can continue to rely on these benefits in retirement. While Social Security remains a cornerstone, it is only one pillar in a well-crafted, goals-based financial plan. At LBDIAS, we believe in aligning your retirement strategy with your unique life vision to support a lifestyle you don’t need to escape from.

Whether you’re days or decades away from retirement, understanding where Social Security fits into your personal Life By Design is an essential first step. To gain perspective on the opportunities and risks, it’s important to explore the program’s history, current challenges, and the smart strategies available to help you navigate your financial journey with confidence.

A Legacy of Support: A Brief History of Social Security

Social Security was established in 1935 during the Great Depression to create a social safety net for aging Americans. What started with modest benefits has become a vital part of retirement income for millions. Today, it also supports disabled workers and families. But like any legacy system, it faces headwinds—especially as our demographic realities shift.

How Social Security Works: Key Facts

To qualify for Social Security, you must be at least 62 and have earned 40 work credits—typically through 10 years of employment. For 2026, one credit is earned for every $1,890 of earnings, with a maximum of four credits per year. Your benefits are calculated based on your highest 35 years of income.

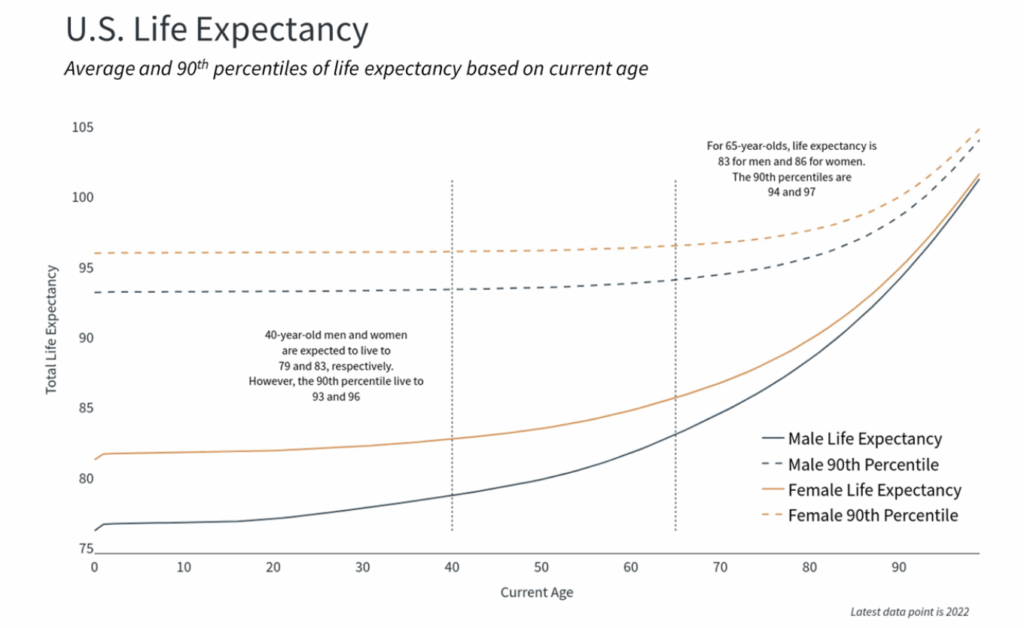

Delaying benefits beyond your full retirement age (67 for those born after 1960) increases your benefit by 8% annually until age 70. This can result in a benefit up to 76% higher than if claimed at 62.

Living Longer, Planning Smarter

Longevity is both a gift and a planning challenge. Social Security operates on a pay-as-you-go system, where today’s workers fund today’s beneficiaries. With a declining ratio of workers to retirees—down from 42:1 in 1940 to about 2.8:1 today—the system is strained. The Social Security Trustees estimate that without reform, reserves could be depleted by 2034–2035, covering only 75–78% of scheduled benefits thereafter.

This underscores the importance of designing a plan that treats Social Security as a supporting role, not the main character, in your retirement narrative.

Working While Receiving Benefits

Many retirees remain inspired to work, but doing so before reaching full retirement age can temporarily reduce your Social Security benefits. In 2025:

- $1 is deducted for every $2 earned over $23,400 (before full retirement age)

- $1 is deducted for every $3 earned over $62,160 (in the year of reaching full retirement age, for earnings before that month)

After reaching full retirement age, you can earn freely without benefit reductions.

Income Taxes on Your Social Security

Up to 85% of Social Security benefits can be taxed depending on your overall income. This includes wages, retirement account withdrawals, capital gains, and other sources. Strategic withdrawal planning is essential to managing your tax bracket and keeping more of your benefits.

Policy Uncertainty and the Global Perspective

National debt, political polarization, and an aging population make solutions elusive. While reforms like raising retirement age or adjusting taxable wage caps are debated, no permanent resolution is in sight. Other nations have faced similar dilemmas: France and the UK have increased retirement ages, and Australia applies a means test to benefits. These international approaches offer insights but also reinforce the importance of personal planning.

The 2034 timeline may feel distant, but at LBDIAS, we know your financial decisions today shape your freedom tomorrow. Our clients are encouraged to prepare proactively—not reactively.

Planning Strategically: Aligning Social Security with Your Life Plan

In a Life By Design retirement strategy, Social Security is a piece of a larger mosaic. Your holistic financial plan—one rooted in your values, purpose, and long-term goals—guides how you approach this benefit.

Key considerations include:

- Delaying with Purpose: Waiting until age 70 to claim benefits can increase your payout significantly. We conduct breakeven and opportunity cost analyses to help you decide what timing best supports your Life By Design.

- Bridge Income Strategies: Using a tailored withdrawal plan from investment portfolios as a bridge to delayed Social Security can be especially valuable—particularly for couples looking to maximize survivor benefits.

- Tax Planning: Up to 85% of Social Security benefits may be taxable. We work with clients to develop personalized, tax-smart withdrawal strategies to preserve more of your benefit.

- Conservative Assumptions for Younger Clients: Younger workers can plan for a retirement that is resilient with or without full Social Security benefits. Our approach: treat benefits as a supplement, not a foundation.

- Stay Policy-Informed: We keep our clients informed of policy changes that could affect their retirement timeline and benefits—helping you stay ahead of adjustments with confidence.

- Maximize Tax-Advantaged Accounts: 401(k)s, IRAs, and HSAs are key components in creating income flexibility and safeguarding your future against uncertainties.

Looking Ahead: A Proactive Path Forward

Social Security has weathered past storms, and it’s unlikely to disappear. But treating it as the only pillar of retirement is risky. At Life By Design, we guide clients in building resilient strategies that reflect not only what they have, but what they envision for the future.

By understanding the role of Social Security in your retirement ecosystem, you gain the clarity and confidence to live intentionally and design a future aligned with your highest goals and values.

Life By Design Investment Advisory Services is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.