A PRACTICAL GUIDE TO TAX EFFICIENT GIVING

For individuals aged 70½ and older, Qualified Charitable Distributions (QCDs) can be a powerful tool, not only for giving back but also for managing taxable income in retirement. Whether you’re motivated by philanthropy or tax strategy, understanding how to use QCDs effectively can enhance your financial plan all year round—not just at year-end.

What Is a QCD?

A Qualified Charitable Distribution allows IRA owners to donate directly from their IRA to a qualified charity, bypassing the traditional tax implications of a distribution.

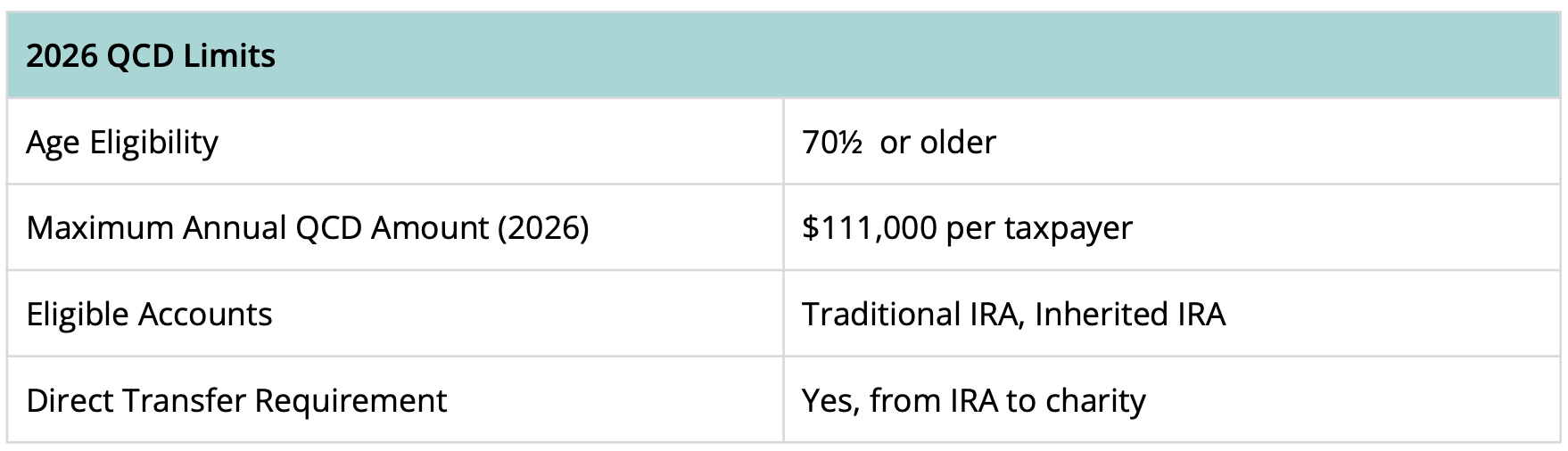

- Age Requirement: You must be age 70½ or older at the time of the distribution.

- Direct Transfer: Funds must be sent directly from the IRA custodian to the charity.

- Qualified Charities: Only donations to 501(c)(3) public charities qualify (excludes donor-advised funds, private foundations, and supporting organizations).

Key Benefits of QCDs

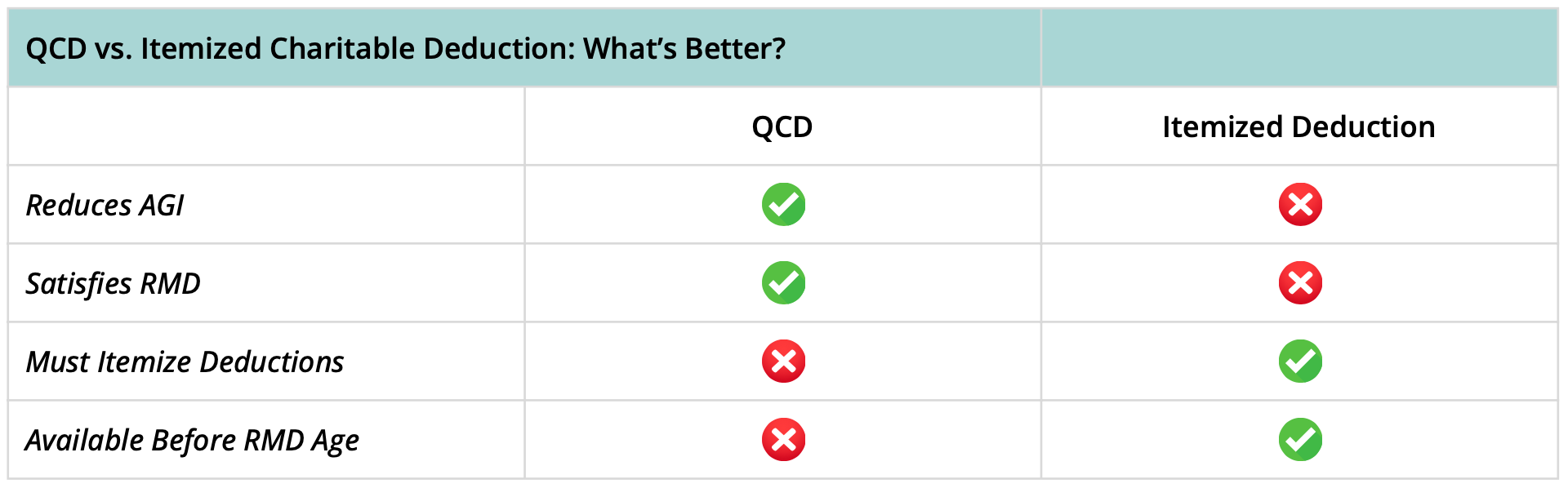

- Tax-Free Giving: QCDs are excluded from your taxable income, which is different from claiming a charitable deduction.

- Satisfies RMD: QCDs count toward your Required Minimum Distribution (RMD), helping you reduce your adjusted gross income (AGI).

- AGI Reduction: A lower Adjusted Gross Income can positively impact your eligibility for tax credits and deductions tied to income levels, including Medicare premiums and tax on Social Security benefits.

Strategic Tips for Using QCDs Year-Round

- Start Early: Don’t wait until December—schedule QCDs throughout the year to smooth out your RMD and reduce risk of error or delay.

- Verify Eligibility: Confirm the charity’s 501(c)(3) status to ensure your gift qualifies.

- Coordinate With Other Giving: Avoid accidental duplication by coordinating QCDs with other charitable gifts (especially those involving appreciated assets).

Other Charitable Strategies to Consider

QCDs aren’t the only charitable tool available. Depending on your tax situation, you might consider:

- Donor-Advised Funds (DAFs): While QCDs cannot fund a DAF, this vehicle allows you to bunch donations and recommend grants over time.

- Charitable Remainder Annuity Trusts (CRATs): Useful for donating appreciated assets while generating income for life.

- Gifting Appreciated Securities: Avoid capital gains tax and receive a deduction for the full market value if itemizing.

- Charitable Bequests: Include charities in your estate plan for future gifts that align with legacy goals.

Documentation and Best Practices

- Keep Records: Obtain an acknowledgment from the charity for your QCD, this is essential for your tax filing.

- Use Correct Forms: Your IRA custodian will issue a Form 1099-R, which may not show the QCD separately. You’ll need to inform your tax preparer.

- Plan Ahead: Integrate QCDs into your overall tax and legacy plan, consult with your advisor to assess their role in long-term giving goals.

At Life By Design, we help clients weave their philanthropic values into their financial plans. Whether you’re using QCDs, DAFs, or creating a family gifting plan, our goal is to align your giving with your legacy.